Everything you need to know about using the value of your Bitcoin long-term without selling it — via Firefish.io or Aave + tBTC — and why it makes far more sense than selling and paying tax.

TL;DR: Don’t sell your Bitcoin. Borrow stablecoins against it (just ~3–4% p.a. via Aave, or via Firefish with fiat straight to your bank account) and spend them with a card or a SEPA transfer. And because a loan is not a sale, you legally pay no tax!

Last updated: June 2026. Interest rates, fees and tax rules change over time — verify the key numbers in the linked sources before you act.

Contents

- Intro: why this still makes sense

- Two philosophies: CeFi vs. DeFi

- Glossary

- Path 1: Firefish.io

- Path 2: Aave + tBTC

- How to turn stablecoins into spendable money (cards, SEPA, peer.xyz)

- How to live off it long-term

- Why it’s legal and when you (don’t) pay tax

- Total cost comparison: Firefish vs. Aave

- Risks you shouldn’t underestimate

- A real-world example

- Summary

- FAQ

Intro: why this still makes sense

My friend Juraj Bednár wrote an excellent mini-course and mini-ebook on this very topic years ago, and I recommend it:

And yet — in 2026, a huge number of people still sell their precious Bitcoin every time they need a bit of cash. By doing so they do two things at once:

- They give up satoshis forever, which no one will give back to them (and of which there will only ever be 21 million).

- They trigger a taxable event — they pay income/capital-gains tax on the difference between the purchase and the sale price (and in some countries additional levies on top).

Selling appreciated BTC, paying tax on it, and then buying Bitcoin back later at a higher price makes almost no sense. There is a more elegant path: don’t sell your Bitcoin — borrow against it. A loan is not a sale, so drawing it triggers no taxable event (more on the tax nuances in a dedicated chapter below).

There are two concrete ways to do this in 2026:

- Firefish.io — the favourite of Bitcoin maximalists who want fiat straight to their bank account and a paper loan contract for the bank.

- Aave + tBTC — a fully on-chain, decentralized path with enormous liquidity and much lower cost.

And because Bitcoin tends to grow faster over time than the interest on the loan, you can live off the loan long-term — you top up or refinance the position as you go, and your Bitcoin stays in your hands.

⚠️ Disclaimer: This is not financial or tax advice. It is a technical how-to. Crypto loans carry real risks (collateral liquidation, volatility, smart-contract risk). Tax consequences depend on your jurisdiction and personal situation — consult a tax advisor before acting.

Two philosophies: CeFi convenience vs. DeFi freedom

| Firefish.io | Aave + tBTC | |

|---|---|---|

| Type | P2P, against native BTC | Fully on-chain DeFi |

| KYC | Yes | No |

| Result | Fiat to your bank account | Stablecoins (USDT/USDC/EURC) |

| Contract for the bank | Yes, they generate it | No |

| Interest | Higher (approx. 5–15% p.a.) | Lower (approx. 3–4.5% p.a.) |

| Liquidity | Limited by lender availability | Enormous |

| Maturity | 3–24 months | None (runs indefinitely) |

| Liquidation | Margin call / top-up from lender | Automatic on-chain at HF < 1 |

| Where your BTC sits | In multisig escrow (non-custodial) | You wrap it into tBTC |

Both paths have their place. If you want paper for the bank (mortgage, proof of funds source) and ready fiat in your account, Firefish is great. If you want the lowest cost, no KYC and maximum control, it’s Aave.

Glossary

A few terms that recur in this article (skip if you already know them):

- Wrap — to “package” Bitcoin into a token on another network (e.g. tBTC on Ethereum) so it can be used in DeFi. The ratio is 1:1 and you can unwrap it back to BTC anytime.

- Collateral — security; the asset (BTC/tBTC) you lock up and borrow against.

- Stablecoin — a token pegged 1:1 to a currency (USDT/USDC = dollar, EURC = euro).

- LTV (Loan-to-Value) — the ratio of the loan to the value of the collateral (LTV 30% = you borrowed 30% of the collateral’s value).

- Health Factor (HF) — the “health” of your Aave position. Above 1 is fine; below 1 means liquidation. The higher, the safer.

- Liquidation — a forced sale of part of your collateral when HF drops below 1.

- Slippage — the difference between the expected and actual rate on a swap; with stablecoins it’s minimal.

- On-ramp / off-ramp — entering crypto from fiat / exiting crypto to fiat.

- Gas — the network transaction fee (higher on Ethereum, low on L2s like Arbitrum/Base).

Path 1: Firefish.io — fiat to your account, contract in hand

👉 Referral link: https://firefish.io?ref=satoshi943

Firefish.io is a non-custodial P2P platform for Bitcoin-backed loans. How it works:

- You go through KYC.

- You lock your Bitcoin into a multisig escrow (it’s not a classic “smart contract” on Ethereum, but a Bitcoin-native multisig between you, the lender and Firefish — no single party holds the keys).

- The platform matches you with a lender who sends you fiat straight to your bank account.

- Firefish generates a loan contract for you — a huge advantage when you need to document the source of funds for a bank or an authority.

Parameters (as of 2026):

- LTV typically ~50% (you lock up roughly 2× the loan value in BTC).

- Interest in the order of 5–15% p.a. depending on the market and lender supply/demand.

- Origination fee 1.5% p.a. of the loan amount, deducted automatically from the BTC collateral when it’s locked.

- Maturity 3–24 months.

- Plus the usual Bitcoin network fees.

Pros: fiat straight to your account, a paper contract for the bank, BTC stays Bitcoin-native (no wrapping onto another network), non-custodial multisig.

💎 Bonus for larger amounts — Auto Invest: Firefish isn’t only about borrowing — if you’re on the capital side, for amounts over €150,000, 100,000 USDC/USDT or 2,000,000 CZK you can activate the Auto Invest program, where the platform invests “for you” (automatically matching and spreading your funds across loans) at noticeably better rates. A nice way to put idle capital to work while you HODL your Bitcoin.

Cons: mandatory KYC, higher interest than DeFi, and the loan is limited by someone on the other side being willing to fund it.

Path 2: Aave + tBTC — the cheapest and freest path

Aave is the largest and most liquid lending protocol in DeFi. It works simply: you deposit collateral → you borrow stablecoins against it. No KYC, no middleman, everything on-chain.

Aave V3 doesn’t run only on Ethereum — it’s deployed on multiple blockchain networks (Ethereum, Arbitrum, Optimism, Base, Polygon, Avalanche, Gnosis and more). On all of these (EVM) networks tokens use the ERC-20 standard, so you first have to “wrap” BTC into ERC-20 form.

Why is Ethereum / ERC-20 recommended? It has the deepest liquidity, the most listed assets, and is the most battle-tested and secure market. The only real downside is higher fees (gas) — so for smaller amounts reach for an L2 network (Arbitrum, Base), where tokens are also ERC-20 but fees are just cents.

There are several ways to wrap BTC (WBTC, cbBTC, LBTC…), but the most decentralized choice is tBTC by Threshold Network.

2.1 Why tBTC (and not WBTC or cbBTC)?

There are several options for wrapping BTC into ERC-20 form — here are the main ones:

- WBTC — historically the most widespread and liquid wrapped BTC, but it’s custodial: a custodian (BitGo and partners) actually holds your BTC. You have to trust that the reserves exist and that no one blocks your access.

- cbBTC — wrapped BTC by Coinbase. Growing fast and with great liquidity, but it’s a fully centralized, custodial solution of a single regulated company (a single point of failure and censorship).

- tBTC — a decentralized bridge by Threshold Network. Both minting and redemption are handled by a group of independent operators via threshold cryptography (threshold signatures), not a single company. No single custodian you have to trust or who can cut you off.

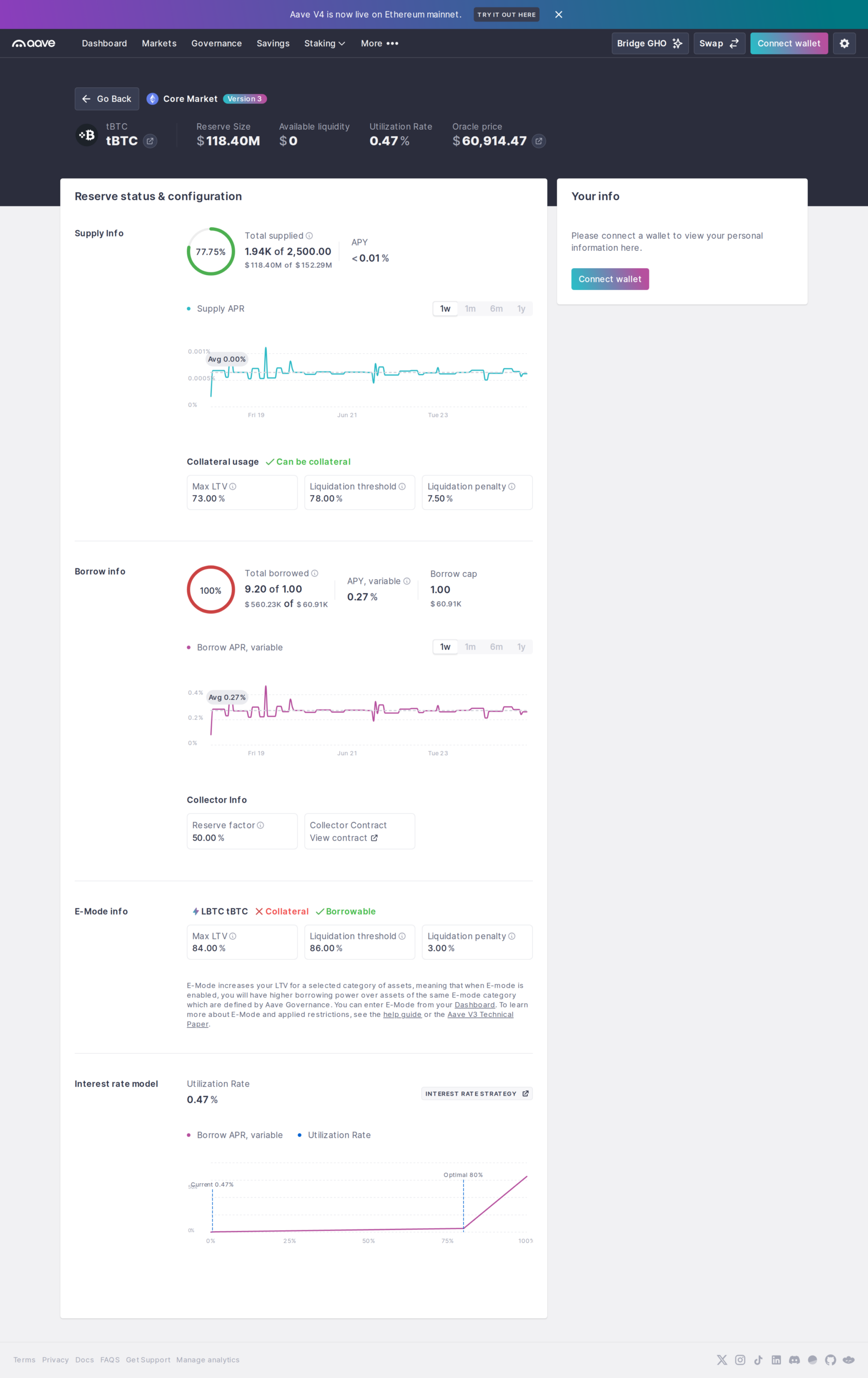

Conclusion: tBTC is the best choice for a bitcoiner who takes “not your keys, not your coins” seriously — it’s the most decentralized while still having sufficient liquidity for practical use. On Aave V3 (Ethereum) tBTC has a reserve size of over $118M (see the screenshot below), so you can comfortably borrow even larger amounts against it. WBTC/cbBTC do have higher liquidity, but at the cost of trusting a single custodian — a compromise that goes against the whole idea of holding Bitcoin.

2.2 How exactly to wrap BTC → tBTC

- Go to the official Threshold / tBTC dApp (dashboard.threshold.network).

- Connect an Ethereum wallet — I recommend Rabby, which is more security-mature than MetaMask (clear transaction previews, warnings about risky signatures, and it clearly shows what exactly you’re signing). This is where your tBTC will land.

- Choose Mint tBTC.

- The app generates a unique deposit BTC address (created via threshold ECDSA, so no single party controls it).

- Send your Bitcoin to that address from your BTC wallet.

- After confirmations on the Bitcoin network you trigger “Initiate minting” in the dApp — once finalized, tBTC is minted to your Ethereum address at a 1:1 ratio.

💡 Fees and a tip about the T token: Minting (BTC → tBTC) is free in 2026 — the minting fee is currently zero. The 0.2% (20 bps) fee is only charged on redemption (tBTC → BTC). In January 2026 Threshold launched stake-based fee waivers: if you have staked the T token, these fees are partially or fully waived (roughly: for every 100,000 T staked, 0.001 tBTC of fees are waived within a rolling 30-day window; the waiver is applied automatically via the Threshold Unified Bitcoin Router). So if you plan to redeem tBTC back to native BTC later, staking T = saved bridging fees.

Note: the precise terminology — the waiver is tied to staking T, not just passively holding it. Verify the current parameters directly in the dApp, since governance can adjust them.

2.3 Depositing tBTC as collateral on Aave

On Aave V3 (Ethereum) tBTC belongs to the BTC-correlated asset group (alongside cbBTC, WBTC, LBTC, eBTC), so it can be used as collateral.

- Go to app.aave.com and connect your wallet.

- Select the Ethereum (Core market) V3 market.

- In the Supply section find tBTC → Supply → enter the amount → confirm (the first time you need to Approve the token, then Supply).

- After depositing, make sure the “Use as collateral” toggle is on.

Fig. 1 — tBTC on Aave V3 (Ethereum): ✓ “Can be collateral”, Max LTV 73%, liquidation threshold 76%, reserve size ~$118.4M (sufficient liquidity). Real screenshot from app.aave.com.

Fig. 1 — tBTC on Aave V3 (Ethereum): ✓ “Can be collateral”, Max LTV 73%, liquidation threshold 76%, reserve size ~$118.4M (sufficient liquidity). Real screenshot from app.aave.com.

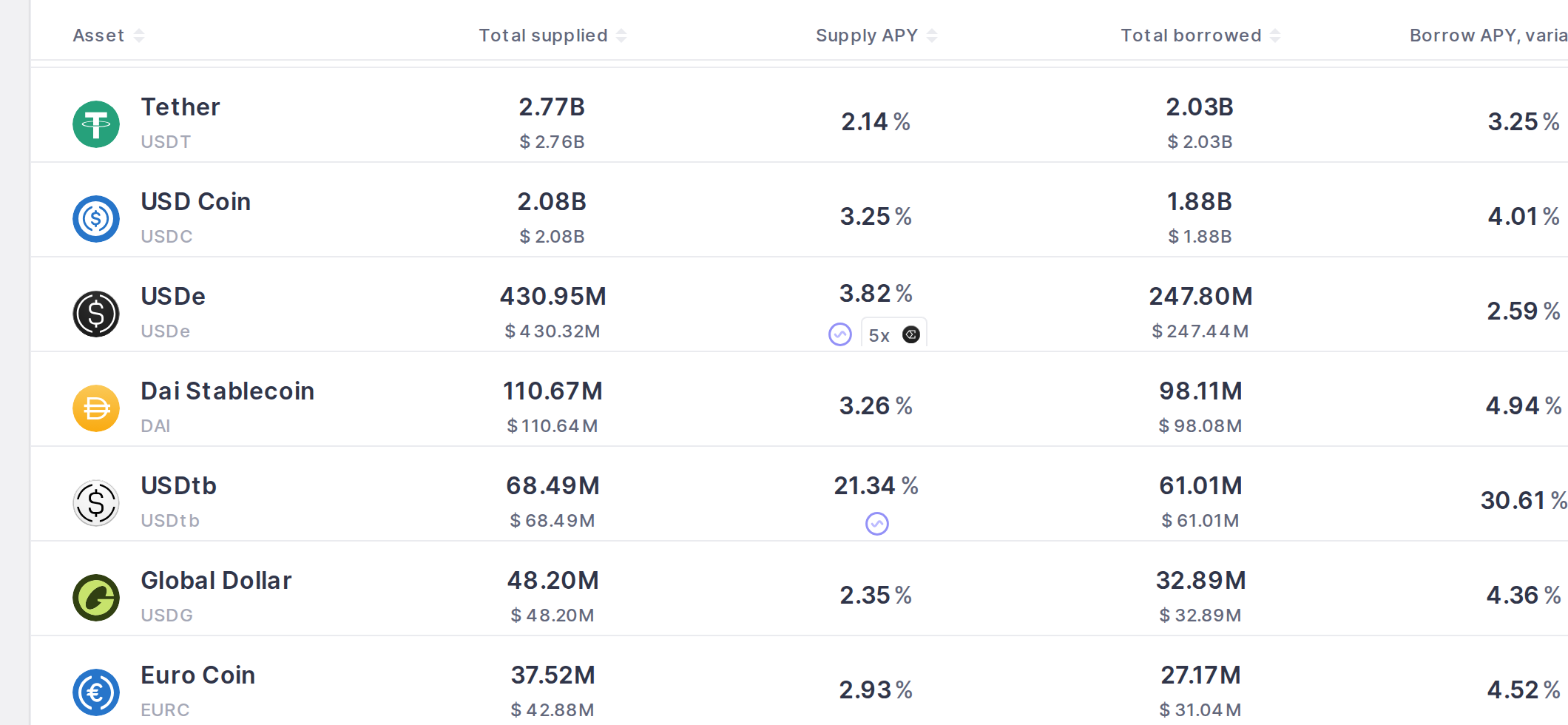

2.4 Choosing a stablecoin and comparing rates (USDT vs USDC vs EURC)

Now you can borrow a stablecoin. The main options are USDT, USDC and EURC. They differ in borrow interest (what you’ll pay) — and that changes with market utilization.

How to compare rates:

- Directly in the Aave app, in the Borrow section, you see “Borrow APY, variable” for each asset.

- In more detail and historically via aavescan.com (e.g.

aavescan.com/ethereum-v3/usdt).

Indicative rates (Ethereum V3, June 2026 — verify current values!):

| Stablecoin | Borrow APY (variable) | Note |

|---|---|---|

| USDT | ~3.3% | Most often the lowest interest |

| USDC | ~4.0% | High liquidity, regulated by Circle |

| EURC | ~4.5% | Euro stablecoin — no FX risk vs EUR |

| DAI | ~4.9% | Decentralized (no central freeze), slightly higher interest |

💡 Practical tip: If your expenses are in euros, EURC removes USD/EUR exchange-rate risk (no need to speculate on the dollar) — and you can spend it directly via ether.fi Cash (EURC deposit and spending with 0% FX on EUR, since May 2026). Note: the other cards (Freedomia, Jeton, Uglycash) are USD-based, so you’d convert EURC to USDC there first. If you just want the lowest interest and FX doesn’t bother you, USDT is usually the cheapest. Always check the current number — rates are variable.

Fig. 2 — Aave V3 (Ethereum) market, an excerpt with the important stablecoins including EURC (Euro Coin) and their supply/borrow APY — compare USDT, USDC and EURC side by side. Real screenshot from app.aave.com/markets.

Fig. 2 — Aave V3 (Ethereum) market, an excerpt with the important stablecoins including EURC (Euro Coin) and their supply/borrow APY — compare USDT, USDC and EURC side by side. Real screenshot from app.aave.com/markets.

2.5 Borrowing and swapping the debt

- In the Borrow section choose your stablecoin (e.g. USDT) → Borrow → enter the amount.

- Important — watch the Health Factor. The more you borrow against your collateral, the closer you get to liquidation. A conservative LTV (e.g. 25–35%, Health Factor well above 1.5–2) gives you a big buffer against a drop in the BTC price.

- Confirm the transaction — the stablecoins are now in your wallet.

Why is it worth knowing how to swap the debt?

- Lower interest — borrow rates are variable and differ between stablecoins; by switching your debt to whichever stablecoin is currently cheaper (e.g. from USDC to USDT) you lower the interest you pay.

- Aligning the currency with your expenses (eliminating FX risk) — if you live in the eurozone, it’s worth holding your debt in EURC; with debt in dollar stablecoins you otherwise carry FX risk (if the dollar strengthens against the euro, your debt grows in euro terms).

- Reacting to the market — if interest on one stablecoin spikes (high utilization) or you have concerns about a particular issuer, you simply move to another.

How to swap: if you borrowed e.g. USDT and want USDC or EURC, you have two options:

- Directly in Aave via the “Swap” feature (Aave has a built-in swap between assets; you’ll find it at your position).

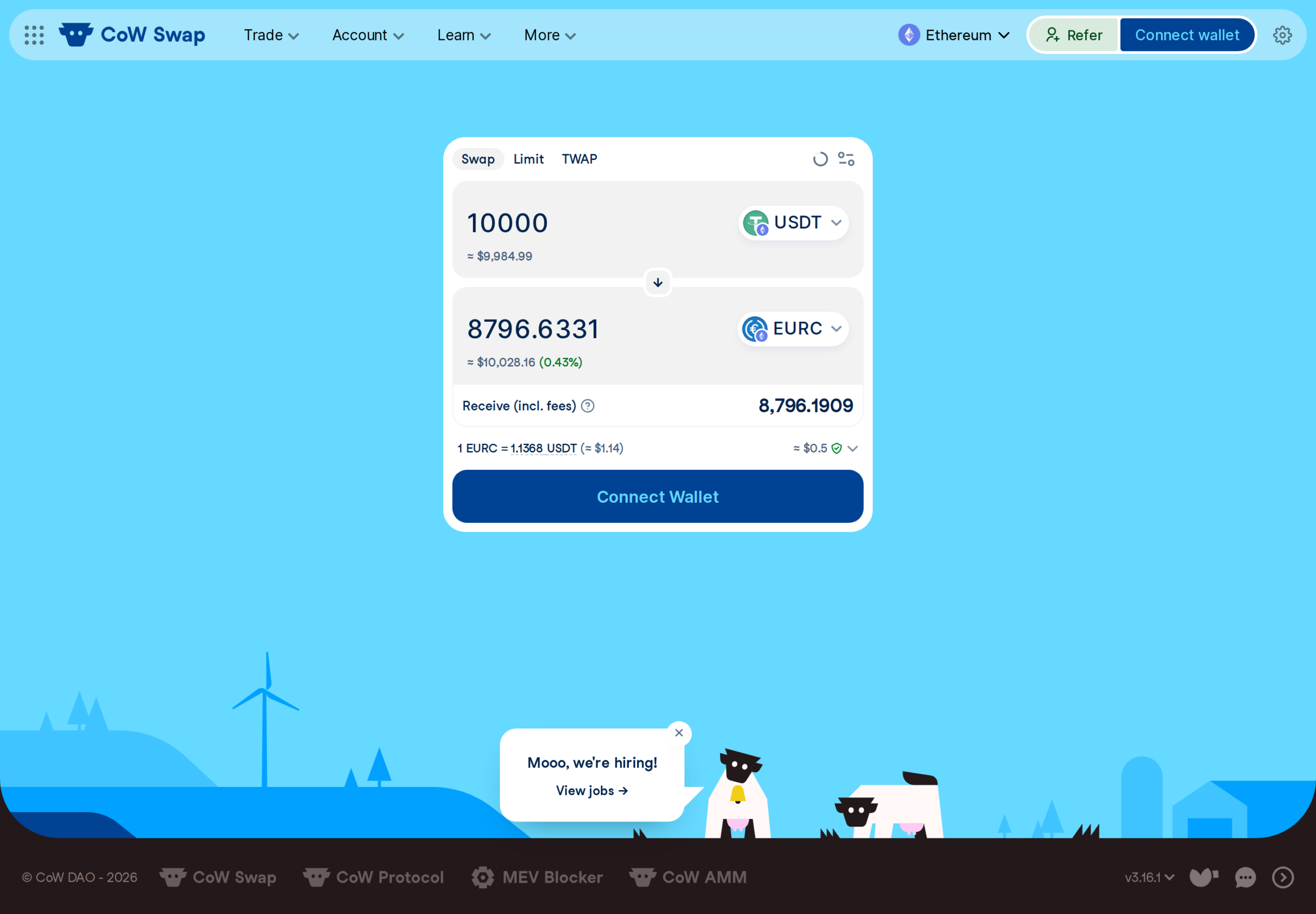

- Or via a DEX aggregator like Uniswap / 1inch / CoW Swap — it finds the best rate across exchanges. For stablecoin↔︎stablecoin swaps the slippage is minimal.

Fig. 3 — Swapping the debt between stablecoins via CoW Swap (10,000 USDT → 8,796.63 EURC, rate 1 EURC = 1.1368 USDT). Real screenshot from swap.cow.fi.

Fig. 3 — Swapping the debt between stablecoins via CoW Swap (10,000 USDT → 8,796.63 EURC, rate 1 EURC = 1.1368 USDT). Real screenshot from swap.cow.fi.

2.6 How to document an Aave loan for accounting / the tax office

The biggest disadvantage of Aave vs Firefish is that it doesn’t generate a paper contract. The protocol is not a legal entity you’d sign a classic “loan agreement” with — and a DeFi loan has no named lender or fixed maturity. A turnkey app that produces a contract like Firefish does doesn’t exist yet. But you can still document the loan for accounting and the tax office — often more convincingly than with paper:

- On-chain proof (the strongest). Every borrow transaction is recorded permanently on the blockchain, and your wallet holds a debt token (variableDebtToken) that says exactly how much you owe. From a block explorer like Etherscan you can export the transaction (hash, date, amount, contract address) as immutable, timestamped proof of the liability.

- Crypto accounting software (audit-ready reports). These tools classify a borrow correctly as a liability, not income, and generate a report for your accountant or the authority:

- Your own statement / internal accounting record. With an accountant (or via a contract generator) you create a document stating that the received funds are a loan — a liability backed by collateral, referencing the on-chain transaction. For a sole trader or company this books the liability correctly.

⚠️ Tax authorities don’t yet have clear guidance on DeFi loans, and in some jurisdictions a DeFi loan may not be treated as a classic “loan”. So always consult a tax advisor or accountant.

2.7 How to guard your collateral: monitoring the Health Factor with Signal notifications

The biggest risk of an Aave loan is liquidation when the collateral price falls. That’s why it pays to monitor your Health Factor automatically and get an alert when it drops below a chosen threshold — you’ll still have time to top up collateral or repay part of the debt. Juraj Bednár wrote a simple open-source solution for exactly this (based on an original script by Brandon Grant):

- jooray/AAVE_Account_Health_Factor — a script (JavaScript) that queries the Aave Pool smart contract directly and reads your address’s current Health Factor. When it drops below a set threshold (default 1.5), it fires an alert.

- jooray/signal-monitoring — a simple monitor that sends notifications via signal-cli straight to the Signal app.

Quick setup:

- Install dependencies:

npm install(needs@aave/core-v3andethers≥ 5.2.0). - In the config set:

userAddress(your address),contractAddress(the Aave Pool contract address for your network — Ethereum, Arbitrum…),jsonRpcUrls(RPC endpoints separated by semicolons) andhealthFactorThreshold(e.g. 1.5). - Connect it to signal-monitoring following the example in the

examples/folder, so a message lands in Signal when it drops. - Run the script regularly — e.g. via cron every few minutes.

💡 Without self-hosting there are alternatives like the Aave Alarm mobile app or Telegram bots, but Juraj’s solution is fully self-hosted and private.

2.8 Repaying and closing the position

You can repay the loan (fully or partially) anytime and withdraw your collateral:

- Get the stablecoin to repay — from income, savings, or swap back what you hold.

- Repay on Aave — in the Borrow section click Repay on the debt, enter the amount (or Max for full repayment) and confirm. You pay the principal + accrued interest.

- Withdraw your collateral — after repaying (or at a sufficiently high Health Factor) click Withdraw in the Supply section and take your tBTC back to your wallet.

- (Optional) redeem tBTC → BTC — via the Threshold dApp you convert tBTC back to native Bitcoin (0.2% fee, which you waive by staking T — see 2.2).

💡 You don’t have to repay everything at once. For “living off the loan” long-term it’s often enough to repay just enough to keep the Health Factor in the safe zone — the rest of the loan keeps running.

How to turn stablecoins into spendable money

Stablecoins in your wallet are nice, but you need to pay with them in shops and send ordinary transfers. That’s what stablecoin / crypto cards are for. A good overview of crypto-friendly services (including ones you can open on a Paraguayan ID card) is in this article.

🪪 Important — a Paraguayan cédula / driver’s license is enough (no passport!): All the stablecoin cards mentioned below (ether.fi, Freedomia, Jeton and Uglycash) can be opened with a Paraguayan ID document / driver’s license only — you don’t need a passport or EU residency. We’re happy to help you obtain a Paraguayan cédula (temporary and permanent residency) — details and up-to-date info here: How to obtain temporary and permanent residency in Paraguay. It opens the door to the whole crypto-friendly infrastructure, including SEPA/IBAN accounts.

The options worth highlighting:

3.1 ether.fi Cash — a non-custodial Visa for DeFi (SEPA/IBAN)

👉 Referral link: https://www.ether.fi/refer/1fb0d559

ether.fi Cash is a non-custodial Visa card (running on the L2 network Scroll) where you hold the keys in your own Gnosis Safe. Two modes:

- Direct Pay — you pay directly with stablecoins (USDC, USDT, EURC, LiquidUSD). Exactly what you borrowed on Aave.

- Borrow mode — you deposit e.g. weETH as collateral and the card borrows a stablecoin on each “swipe”; your ETH keeps earning staking yield in the meantime.

Practical parameters: no annual fee, 0% FX on EUR and USD transactions (1% elsewhere), cashback in wETH/ETHFI, ATM withdrawals up to $250/transaction (2%, max 3×/24h). KYC required.

How to get stablecoins in and spend:

- Sign up via the referral link above and complete KYC.

- In the app choose Add Funds → send USDC/USDT/EURC from your wallet (the one you borrowed into from Aave) to the deposit address shown on the correct network.

- Activate the card (virtual instantly, plastic on request) and pay directly with stablecoins or via Borrow mode.

📌 SEPA: besides the card with 0% FX on EUR, ether.fi also supports SEPA/IBAN — so you can not only spend stablecoins with the card but also send them via an ordinary transfer. You open it on a Paraguayan cédula.

3.2 Freedomia — a no-KYC Visa, topped up with stablecoins

👉 Referral link: https://freedomia.io/a/h64xqa

Freedomia is a prepaid no-KYC Visa card you top up with Bitcoin (incl. via Lightning), USDT, USDC or ETH. Ideal as a fast, private card for everyday spending.

How to:

- Sign up via the referral link above.

- Create a card and, in the top-up section, send USDT/USDC (or BTC via Lightning) to the address shown.

- Once credited, pay with the card like an ordinary Visa.

📌 Note on SEPA: Freedomia is a top-up card, not a SEPA/IBAN account — don’t expect to send classic SEPA transfers through it. Its strengths are privacy (no KYC) and simplicity. For SEPA transfers use ether.fi or Jeton (below).

3.3 Jeton — a stablecoin card with full SEPA/IBAN

Jeton is an excellent choice when you need real SEPA transfers via your own IBAN. KYC on a Paraguayan cédula / driver’s license takes a few minutes, and you keep the account in USD or EUR (optionally another currency too).

Why it fits this purpose:

- Free crypto/stablecoin top-up — you send USDT/USDC (ERC20/TRC20/Solana), or BTC/ETH and others.

- Full SEPA/IBAN — outgoing SEPA transfers in your name with no fee, usually credited the next day. FX/conversion at roughly the mid-market rate (around ~0.2% + 0.5% FX).

- A multi-currency card for everyday spending.

How to:

- Sign up and complete the quick KYC (Paraguayan cédula/driver’s license).

- Send USDT/USDC to your Jeton crypto address (top-up is free).

- Convert to EUR and either pay with the card or send a classic SEPA transfer to any bank account.

3.4 Uglycash — an eUSD account with IBAN, SEPA and a Visa card

👉 Referral link: https://applink.ugly.cash/referral/wilderko

Uglycash is a regulated fintech app built on the eUSD stablecoin (always = 1 USD). It gives you a European IBAN, a US account/routing number, and a Visa debit card all at once — and you open it on a Paraguayan cédula.

Why it’s handy:

- Multiple top-up methods — crypto (USDT, USDC, BTC, ETH) and ordinary bank transfer/wire.

- Your own IBAN → you send and receive SEPA transfers; withdraw back to a bank via SEPA/ACH.

- A Visa card (virtual instantly, plastic on request) for everyday spending; eUSD is converted automatically to the local currency at payment.

How to:

- Sign up via the referral link and complete KYC (Paraguayan cédula/driver’s license).

- Send USDC/USDT from your Aave wallet to your Uglycash crypto address → it’s credited as eUSD.

- Pay with the card or send a SEPA transfer from your IBAN to any account.

💡 Cards summary: ether.fi Cash (non-custodial, 0% FX EUR, EURC), Freedomia (no KYC, privacy), Jeton (strong SEPA/IBAN), Uglycash (IBAN + US account + SEPA). For pure spending any of them will do; for SEPA reach for Jeton, Uglycash or ether.fi; for EURC with no FX reach for ether.fi.

🏦 Bonus: you don’t need an EU bank account. Since you can make full SEPA transfers through stablecoin services with their own IBAN (Jeton, Uglycash, ether.fi), you no longer need a classic EU bank account for everyday sending and receiving — stablecoins replace it in practice.

3.5 peer.xyz — borrowed USDC straight to your bank account (no KYC)

If you don’t want a card but fiat straight to your bank account (Revolut, Wise, N26 and others), a great choice is peer.xyz — a trustless P2P exchange built on the ZKP2P protocol (by P2P Labs). It lets you safely and without KYC exchange your borrowed stablecoins (USDC) for fiat that a counterparty sends straight to your account.

How exactly it works (and why it’s safe):

- Escrow in a smart contract. Your USDC is locked into an on-chain smart contract (on Ethereum) — not at any company. No one can touch it until the condition is met (fully non-custodial).

- Matching and the fiat payment. The protocol matches you with a counterparty (a liquidity provider) who sends fiat straight to your bank account (Revolut, Wise, N26, SEPA…). You pick the payment method you normally use.

- Cryptographic proof of payment. That the fiat really arrived is verified by the protocol via a proof (zkTLS / zkEmail / TEE) — mathematically, not by trust. Verification via TEE now takes under a second.

- Releasing the USDC. After the payment is verified the smart contract automatically releases the locked USDC to the counterparty. You already have the fiat in your account. The whole thing takes seconds.

Why it’s advantageous: no KYC and no storage of personal data (“zero data stored”, powered by zero-knowledge proofs), no middleman (market, fair rates), money straight into the bank you already have. Counterparty risk is handled precisely by that escrow + proof of payment — hence “built on proofs, not promises”.

⚠️ Note: peer.xyz is a newer project (in BETA at the time of writing), younger than the established cards. On first use start with smaller amounts and proceed carefully.

💡 So together with the SEPA cards (Jeton, Uglycash, ether.fi) you have a choice: spend with a card, send SEPA transfers, or get fiat straight to your bank account via peer.xyz — all without selling a single satoshi.

How to live off it long-term: refinancing and topping up

The title of this article promises living off the loan long-term — here’s how it works in practice:

- Bitcoin rises → your LTV falls. If you borrow at LTV 30% and the BTC price rises, the value of your collateral grows and the debt-to-collateral ratio falls on its own (Health Factor rises). The position “self-heals” over time.

- Top-up. When the LTV drops, you can draw another loan against the same BTC — again without selling and without tax. So you keep pulling cash out of your appreciating Bitcoin, for years.

- Refinancing. Interest is variable — when rates drop or a cheaper stablecoin appears, you “swap” your debt (see 2.5). On Aave you also never have to “renew” the loan (it has no maturity), so the repeated origination fee you’d pay at Firefish disappears.

- Deleverage when needed. In a bear market or at a higher LTV, repay part of the debt or add collateral so you never get close to liquidation. The goal is to survive even a 70–80% price drop.

- Watch out for the growing debt. If you never repay anything, interest keeps accruing onto the debt and your Health Factor can fall even without a drop in the BTC price. So at least occasionally repay the accrued interest or keep a reserve — otherwise even a “calm” position catches up with you after a few years.

⚠️ Discipline is everything. “Living off the loan” works as long as you don’t overdo the leverage. Conservative LTV + monitoring the Health Factor (see 2.7) + a reserve to top up = a good night’s sleep even in volatility.

Why it’s legal — and when you (don’t) pay tax

The key idea of the whole concept:

A loan is not a sale. When you draw a loan, no “income” flows to you — you receive someone else’s money that you have to pay back. So drawing the loan itself is not a taxable event and triggers no income or capital-gains tax.

When you sell 1 BTC for €60,000 (illustrative price) that you bought for €15,000, you have a €45,000 gain and you pay tax on it. When you instead borrow €20,000 in stablecoins against that same BTC (LTV ~33%), you’ve sold nothing — the BTC is still yours (just locked as collateral) and the borrowed money isn’t income. No realized gain = no tax at that moment.

But be honest and careful (caveats):

- Liquidation = a sale. If BTC drops and your collateral is liquidated, that IS a disposal of the asset and therefore a taxable event. So keep your LTV conservative.

- Repaying and closing the position may have its own tax consequences (FX differences on stablecoins, etc.).

- Loan interest is usually not deductible for an individual.

- Rules differ and change. This is a general principle, not individual advice. Consult a tax advisor for your specific situation and jurisdiction.

The point: the legal logic “borrow instead of sell” is exactly what wealthy people do with stocks and real estate (buy, borrow, die). It works with Bitcoin too — and often more cheaply.

Total cost comparison: Firefish vs. Aave

Model example: a loan worth €50,000 for 1 year.

Firefish.io

| Item | Cost |

|---|---|

| Interest (roughly ~9% p.a.) | ~€4,500 |

| Origination fee 1.5% p.a. | ~€750 |

| BTC network fees | a few € |

| Total for the year | ~€5,250 → approx. 10.5% p.a. |

Aave + tBTC (borrowing USDT)

| Item | Cost |

|---|---|

| Borrow interest USDT ~3.3% p.a. | ~€1,650 |

| Minting BTC → tBTC | €0 (free) |

| Gas (supply/borrow/swap) | one-off ~tens of € |

| (Optional) card withdrawal / FX | ~0–1% |

| Total for the year | ~€1,700 → approx. 3.4% p.a. |

Verdict: at current rates Aave + tBTC is roughly 3× cheaper than Firefish (approx. 3–4% p.a. vs. ~10% p.a.). For the higher cost at Firefish, though, you get fiat straight to your account and a paper contract for the bank, and you don’t have to deal with on-chain operations. Aave is the choice for someone who wants the lowest cost, no KYC and full control — in exchange for managing the Health Factor and liquidation risk themselves.

And over 5 years? An Aave loan runs indefinitely, so you only pay interest (~3–4% p.a.). Firefish has a maturity of 3–24 months, so it must be renewed repeatedly and you pay the 1.5% origination every time again. For a €50,000 loan over 5 years that’s roughly Aave ~€8,000–10,000 vs Firefish ~€26,000 and more (interest + repeated origination). The longer you “live off the loan”, the bigger the difference.

Note: the numbers are indicative as of June 2026. Aave rates are variable — always verify the current rates at app.aave.com / aavescan.com before borrowing.

Risks you shouldn’t underestimate

- Collateral liquidation on a sharp drop in the BTC price → keep LTV low, keep a reserve to top up/repay, and monitor the Health Factor with Signal alerts (see 2.7).

- Smart-contract risk (Aave, the tBTC bridge) — even though these are mature, audited protocols.

- Bitcoin volatility — a loan against a volatile asset requires discipline.

- Stablecoin risk — de-peg and freezing. Centralized issuers USDC (Circle), USDT (Tether) and EURC can freeze or blacklist an address. If censorship resistance matters to you, consider the more decentralized DAI (MakerDAO/Sky), which has no central freeze switch at the token level — in exchange for slightly higher interest.

- Self-custody responsibility — your keys, your responsibility (and your mistakes).

- Use a hardware wallet (Trezor, Keystone, Ledger) as the signer and Rabby only as the interface — for larger amounts it’s a must.

- Test with a small amount first — try the whole flow (mint 0.01 BTC → supply → borrow a few €) with a minimum before you send a large amount.

At what price drop do you get liquidated? (tBTC liquidation threshold = 76%)

| Your LTV | Health Factor | BTC can drop by |

|---|---|---|

| 25% | ~3.0 | ~67% |

| 30% | ~2.5 | ~60% |

| 40% | ~1.9 | ~47% |

| 50% | ~1.5 | ~34% |

| 60% | ~1.3 | ~21% |

So a conservative LTV (25–35%) survives even a brutal bear market; at a high LTV even a mild drop will liquidate you.

A real-world example

Marek has 2 BTC (at an illustrative price of ~€60,000/BTC) and needs €20,000 for a renovation. He doesn’t want to sell them — he’d lose satoshis and also pay tax.

- Wrap: he sends 1 BTC to the Threshold dApp and mints 1 tBTC (minting is free). He keeps the second BTC in cold (hardware) storage.

- Collateral: he deposits 1 tBTC (~€60,000) on Aave as collateral.

- Borrow: he borrows €20,000 in EURC (debt and expenses both in euros = no FX risk) → LTV ~33%, Health Factor ~2.3 (safe even in a big drop).

- Spending: he sends the EURC to ether.fi Cash and either pays directly with the card (0% FX on EUR), or sends euros to the contractor via a SEPA transfer from ether.fi.

- Guarding: he sets up Juraj’s script (2.7), which sends him a Signal alert when the Health Factor drops below 2.

- Long-term: as BTC rises, the LTV falls; Marek either repays the loan from income or, at a higher price, draws more cash — still without a single sale and without a taxable event.

Cost: €20,000 at EURC ~4.5% p.a. costs him ~€900 per year — a bit more than the cheapest USDT (~3.3%), but with no USD/EUR FX risk; even so it’s a fraction of the tax he’d pay on selling appreciated BTC.

Summary

- Selling appreciated Bitcoin and paying tax on it is, in the vast majority of cases, unnecessary. There’s a better way: borrow against it.

- Firefish.io = convenience, KYC, fiat to your account + a contract for the bank, higher interest (~5–15% p.a., + 1.5% origination).

- Aave + tBTC = the cheapest and freest path. You wrap BTC into decentralized tBTC (minting is free; by staking T you save on redemption fees), deposit it as collateral, borrow USDT/USDC/EURC (~3–4.5% p.a.) and compare rates via the Aave app / aavescan.

- Spending and SEPA: send the stablecoins to a card — ether.fi Cash (non-custodial Visa, 0% FX EUR, SEPA), Freedomia (no-KYC Visa), Jeton (strong SEPA/IBAN) or Uglycash (IBAN + US account + SEPA) — or get fiat straight to your bank via peer.xyz.

- 🪪 All these cards can be opened with a Paraguayan cédula/driver’s license only (no passport) — and we’re happy to help you get Paraguayan residency.

- Tax: drawing a loan is not a sale → no taxable event arises at that moment. Beware of liquidation (= a sale) and always consult a tax advisor.

- Cost: at current rates Aave is ~3× cheaper than Firefish (~3–4% vs ~10% p.a.).

Bitcoin is the hardest money humanity has ever had. Don’t spend it — borrow against it and let it keep working.

Where to start? If you want convenience and paper for the bank, go via Firefish. If you want the lowest cost and full control, choose the Aave + tBTC path. And if you need help with Paraguayan residency or setting up the whole stack, get in touch with us.

FAQ

1. When do I have to repay an Aave.com loan? (applies to: Aave)

There’s never a fixed repayment date. Unlike a bank loan or Firefish (where you have a 3–24 month term), an Aave loan has no fixed maturity (no date by which it must be returned) — it runs until you repay it yourself. You can repay (in full or in part) anytime. The only condition is that you must keep a healthy position (Health Factor above 1): interest accrues onto the debt over time, and if the collateral value falls (or the debt grows) enough that the Health Factor drops below 1, the protocol liquidates you automatically (it sells part of the collateral to repay the debt + a penalty). Rule of thumb: keep a reserve, watch the Health Factor, and if the BTC price drops either add collateral or repay part of the debt.

What Health Factor to keep? In a calm/rising (bull) market a HF of 1.8–2.0 usually suffices; in a volatile/falling (bear) market keep 2.5–3 and above — the higher the number, the bigger the buffer against a price drop and the better you sleep. Very conservative users keep their Health Factor above 3 permanently.

2. How does the dynamic interest rate work? (applies to: Aave)

Aave uses a variable (dynamic) interest rate driven by market utilization — i.e. the ratio of how much of the deposited asset is currently borrowed:

- Low utilization → low interest (plenty of money, it’s “cheap” to borrow).

- High utilization → high interest (liquidity is scarce, the rate rises to motivate repayment and new deposits).

The model has an optimal point (kink) — up to it the rate rises gently, beyond it steeply. The rate is recalculated practically block by block, so what you pay changes over time. That’s why you should watch the current “Borrow APY, variable” in the app or at aavescan.com before and during your position. This dynamic is exactly why some stablecoins (e.g. USDT) tend to be cheaper than others.

3. How can I swap the debt between several stablecoins? (applies to: Aave)

There are two levels — don’t confuse them:

- Swapping the tokens you hold in your wallet (you borrowed USDT but want to spend EURC): you simply exchange them via a DEX aggregator (CoW Swap, Uniswap, 1inch) — for stablecoin↔︎stablecoin the slippage is minimal (see Fig. 3). Your debt in Aave, however, stays denominated in the original asset (USDT).

- Swapping the debt itself (you want your whole loan to cost EURC interest instead of USDT): there’s a feature directly in Aave, “Swap borrowed amount” / debt switch, which changes the currency of your debt (useful when another stablecoin has lower interest or you want to align the debt currency with your expenses, e.g. EUR).

Tip: if you live in the eurozone, consider holding both the debt and your spending in EURC to avoid USD/EUR FX risk.

4. Is there a minimum deposit to use this lending system? (applies to: Aave and Firefish)

Aave has no formal minimum — technically you can deposit even a few dollars. The real constraint is transaction fees (gas) on Ethereum: for small amounts, minting tBTC, supply, borrow and swap eat up a disproportionate amount, so it practically pays off from a few thousand EUR upwards. If you go with smaller amounts, use a cheaper network (an L2 like Arbitrum or Base), where fees are cents. Note: Firefish does have its own minimum loan amounts (usually higher), so for small amounts Aave on an L2 is usually more accessible. With the tBTC path the upper limit is set only by how much tBTC you deposit as collateral; the only formal minimum is minting tBTC from 0.01 BTC (range 0.01–10 BTC per mint).

5. Do I have to pay tax on this? (applies to: Aave and Firefish)

Drawing a loan itself is not a sale, so no taxable event arises at that moment — you don’t receive “income”, just someone else’s money that you’ll return (see the chapter Why it’s legal — and when you (don’t) pay tax). This is the main advantage of the whole concept. But beware of situations that may be taxable:

- Liquidation of collateral = a forced sale of your BTC/tBTC → a taxable event.

- A swap between cryptos (e.g. tBTC↔︎BTC, or stablecoin↔︎stablecoin) may be treated as a taxable exchange in some jurisdictions.

- FX differences on stablecoins when repaying.

This is not tax advice — rules differ by country and change over time. Consult a tax advisor for your specific situation.

6. Can I use Monero (XMR) or Zcash (ZEC) as collateral? (applies to: Aave)

Not directly — neither XMR nor ZEC is an ERC-20 token, and Aave (on Ethereum/L2) doesn’t recognize them. You first have to exchange them for an asset Aave supports (ETH, a stablecoin, or tBTC/wBTC) and then deposit that as collateral. The most advantageous and at the same time private way:

- Best rate via an aggregator: Trocador.app compares the rates of 20+ no-KYC/low-KYC exchanges at once, with no extra aggregator fee and a colour-coded “KYC risk” rating — pick the best offer (note: it prohibits use by US residents).

- Conveniently from a wallet: Cake Wallet / Monero.com have a built-in swap (via providers like ChangeNOW).

- Fully decentralized (no middleman): cross-chain DEXs like THORChain / Maya Protocol; for maximum privacy with XMR, the P2P exchange Haveno.

Recommended flow (lowest cost):

- Via an aggregator, exchange XMR/ZEC → the target asset right on a cheap L2 (Arbitrum/Base) to save on gas — ideally into what you want to hold long-term: ETH or BTC → tBTC (so you can borrow stablecoins against it as in the main guide). If you just want conservative collateral, USDC/USDT works too.

- Deposit the target asset as collateral on Aave and continue as in chapters 2.3–2.5.

Tips for value: privacy coins tend to have a wider spread, so it pays to compare rates (Trocador) and possibly split larger amounts into several smaller swaps; with ZEC send from a shielded address where possible. Count on this being one extra conversion step (spread + exchange fee) compared with already holding BTC/ETH.

Related on Liberation Travel

- Why TBC Bank in Georgia is crypto-positive — and how to actually move crypto in and out

- Crypto-friendly services you can open with just a Paraguayan ID card / driver’s license

- How to obtain temporary and permanent residency in Paraguay

This article is for educational purposes and is not financial or tax advice.